Transfer Tax Safe Harbor for Certain Trump Accounts

IRS Revenue Procedure 2026-25 creates a safe harbor that allows qualifying contributions to Trump accounts to qualify for the annual gift tax exclusion without requiring Form 709 filing. The guidance reduces compliance burdens for donors and the IRS.

By Aaron Klein, CPA-East Texas

IRS Revenue Procedure 2026-25 introduces a targeted transfer tax safe harbor that resolves significant compliance uncertainties created by the new Trump accounts under Section 530A.

Prior to this guidance, contributions to these accounts – where the minor beneficiary generally cannot access funds during the growth period – would typically be classified as gifts of future interests. This would disqualify them from the annual gift tax exclusion and require filing Form 709 for many donors, even those far below the lifetime exclusion/GST exemption thresholds ($15 million for 2026). With millions of accounts already opened, this could have generated millions of additional gift tax returns, creating substantial burdens for both taxpayers and the IRS.

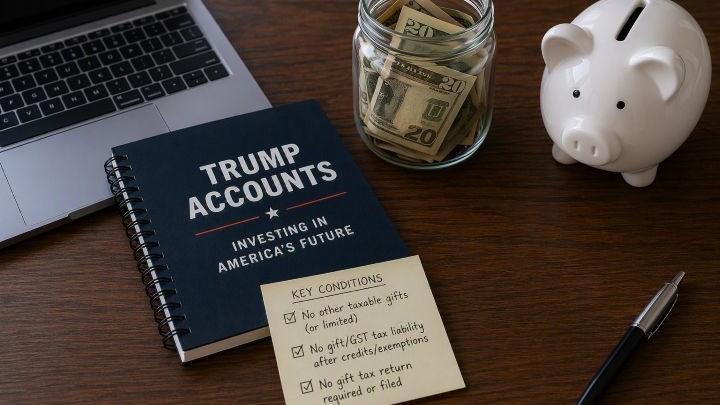

Rev. Proc. 2026-25 changes this by providing a safe harbor under which qualifying cash contributions by individual donors are treated as completed gifts that are not future interests and are eligible for the annual per-donee exclusion. Key conditions include:

- The donor makes no other taxable gifts (or limited ones not exceeding the exclusion per beneficiary),

- The contributions create no gift/GST tax liability after applicable credits/exemptions, and

- No gift tax return is otherwise required or filed for the year.

When met, donors avoid Form 709 reporting for these contributions entirely. The Rev. Proc. includes an illustrative example, recordkeeping reminders and applies for calendar years meeting the criteria, offering immediate practical relief effective June 29, 2026.

Also see: IRS says Trump Account contributions will not trigger annual gift tax reporting requirements

Topics: